This data insight is a two-part analysis of the impact of AI and changing views of the value of Software as a Service on early-stage investing. Part 1 reviews the pros and cons of the “SaaSpocalypse” and its impact on software valuations, exits and potential investor returns. Part 2, coming next month, will suggest how angels and other early-stage investors should deal with changes in the software investing landscape.

SaaSpocalypse Now?

Mark Andreessen famously argued that “Software is eating the world.” Fifteen years later, AI began eating software.

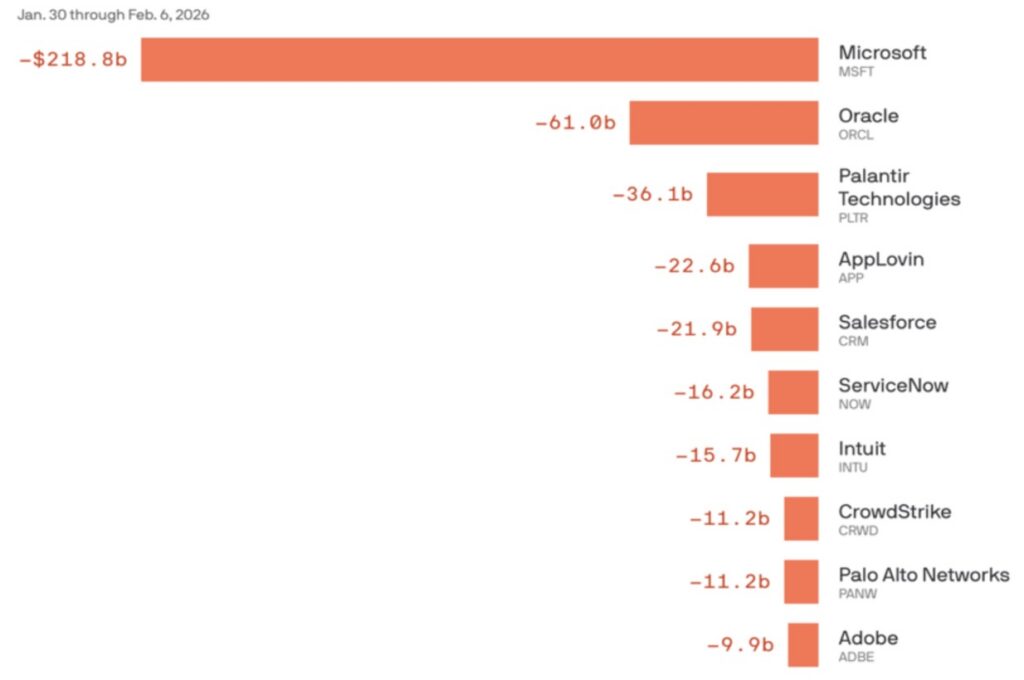

In Q1 2026, Wall St. turned sour on SaaS, initially, on reports that top tech companies were replacing programmers with AI coding. The “Saaspocalypse,” named by Jeffries’ trader, Jeffrey Favuzza in February, seemed to some to herald the end of the glory days of Software as a Service. SaaS comprises about 80% to 90% of all venture or angel-backed business software companies. In reaction to the threat of AI, February saw an unprecedented decline in the value of the software sector in just one week. (Figure 1)

Figure 1: Market Cap Losses for Select Software Companies

Source: Axios Visuals

Wall Street embraced SaaS enthusiastically. Finally, we have believable and predictable revenue forecasts thanks to sticky, recurring per-seat revenues! But with agents replacing human coders, and longer-term, replacing corporate workers with autonomous decision-making agents, Saas’s per-seat virtue became a vice. With the rise of agentic computing, analysts not only forecast the end of seat-based revenues, as tech companies shed human developers, they also forecast custom agentic-powered workflow replacing many of the complex enterprise workhorse applications themselves. Who needs expensive enterprise systems when you can code them yourself?

The sell-off during the first week in February was triggered by Wall Street’s reaction to the mid-January release of Claude Cowork targeting enterprise workflows, and then, more severely at the end of the month when Cowork plug-ins targeted human labor in finance, HR, sales and legal. Here was irrefutable proof of analysts’ long simmering fears about AI’s impact on SaaS economics. It was no longer a vague, future threat, but a fast-emerging reality. Dump SaaS stocks before the SaaSpocalypse hits!

During the first week in February, software stocks lost $300B in value. By the end of March Atlassian was down 58%, Workday and Hubspot were down nearly 40%, and Adobe was down by more than 30%. Overall, Q1’26 saw the largest decline in software values in thirty years. The S&P Software Index fell by 20% during February. (Figure 2) And the Software Equity Group’s (SEG) SaaS Index declined by 26% as of March 31. Overall sector damage has been estimated at one to two trillion dollars of lost value.

Figure 2: S&P North American Technology Software Index

Source: R Weissman’s analysis of S&P 500 Software Index Data

The predictions have remained, but the feared collapse in SaaS per-seat revenue has not yet transpired, in part because the enterprise market is only mid-way through its urgent transition to the Cloud.

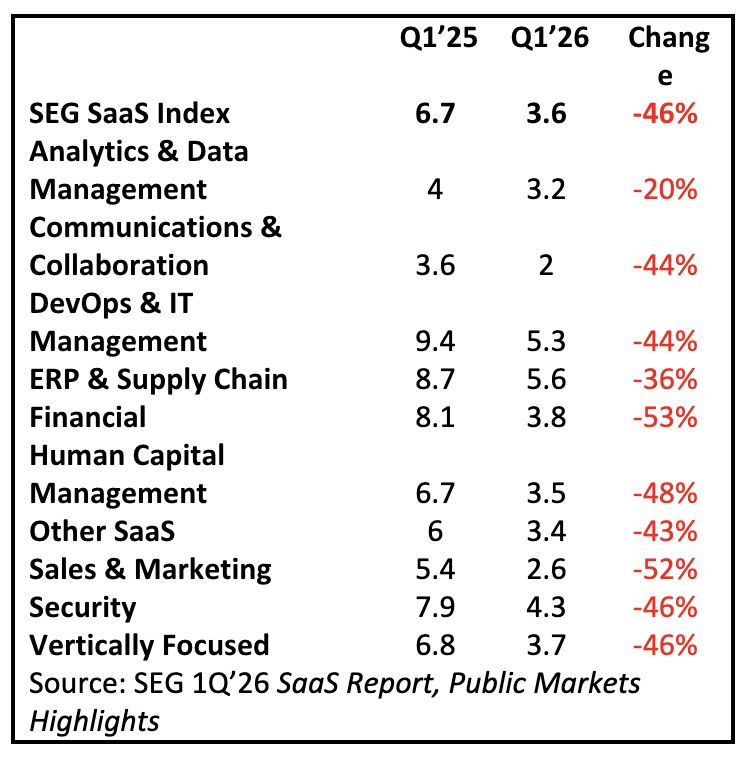

While SaaS revenues themselves have not yet declined, YoY Q1 2026 SaaS valuation multiples have taken a significant hit. (Figure 3) Every subsector measured by The Software Equity Group (SEG) has declined, most by about 50%. Not surprisingly, since data has emerged as a powerful moat, data management and analytics have suffered the least valuation decline. Nevertheless, lower multiples eventually affect markets more broadly as they usually translate into lower valuations for new financing rounds and lower exit values for investors.

Figure 3: Change in Median EV / TTM Rev. Multiple, Q1’25 vs. Q1’26

Source: SEG 1Q’26 Saas Report, Public Markets Highlights

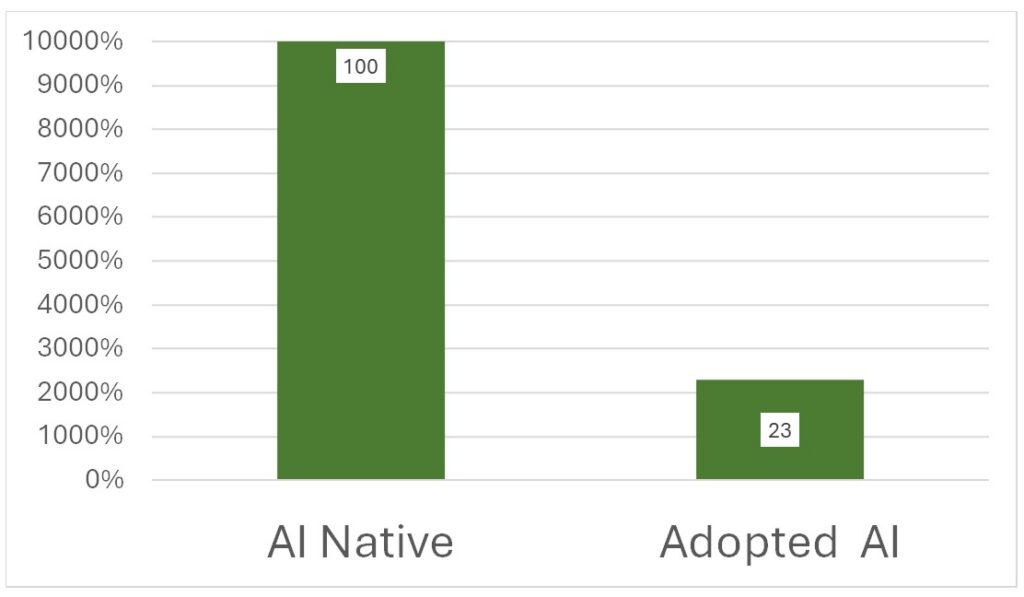

While revenues are still growing, the long-term outlook for SaaS is weaker, as revenue growth rates are slowing, particularly when compared to AI native software. Emergence Capital’s recent benchmark report suggests that AI-native companies are growing 4.3 times as fast (Figure 4) as traditional SaaS having merely after the fact (adopted) bolt-on AI.

Figure 4: 2024 % ARR Median Growth Rate By Company Type

Source: Emergence Capital, Beyond Benchmarks, 2025

Deepstar Strategies (11/16/25) attributes these differences in growth rates to the different work performed by SaaS compared to AI-Native solutions. SaaS manages workflow. Native AI manages decisions. In the era of agentic AI, AI native applications make decisions enabling immediate action, rather than providing data to better manage workflow.

While software revenues continue to grow, troubling signs are emerging as valuations continue to shrink and installed base revenues (the percentage of total revenues from the installed base as measured by net recurring revenues, NRR) are now at their lowest in many years, most recently amounting to only 106% of revenues, down from 117% in 2021 (Software Equity Group SaaS index, as reported by Long Angle Investments, Software vs. AI, Q1 2026.) Installed base revenues often are seen to anchor a company’s financials in a company’s often most dependable segment, its existing customers. Declining NRR usually indicates emerging problems in one’s installed base.

Overall annual SaaS revenue growth rates have slowed over the past several years. It is anticipated that the shift to agentic computing will accelerate this decline. Buyers and vendors of SaaS software both indicate a fear that AI will quickly commoditize SaaS, reduce differentiation, harm margins and reduce long-term vendor viability. These trends will likely reduce the value of those SaaS companies waiting to exit investor portfolios.

Figure 5 compares the decline in growth rates for private software companies from 2020 to 2024. As the chart reveals, every revenue band has seen declining revenue growth rates, with later stage companies achieving growth of approximately 20%. As will be discussed later, in the current exit market IPO eligibility typically requires 30% or greater revenue growth.

Figure 5: Median Growth of Private Software Companies by ARR

Source: SaaS Capital, 2025 Private B2B SaaS Company Growth Rate Benchmarks.

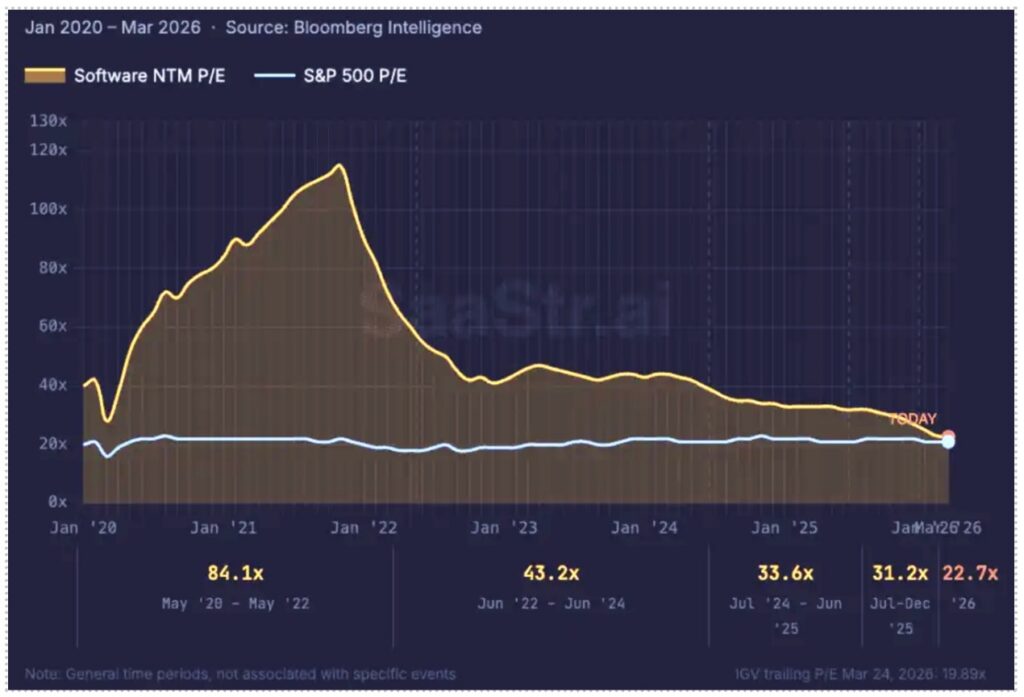

For public companies, there is a similar expectation of slower growth. Translated into economic value (P/E ratios), the picture is one of a constant decline (See Figure 6) from a multiple of 84x during the 2021 bubble, then cut in half (43x) post-Covid. Multiples fell again to 33x in January ‘26 before the SaaSpocalypse, and then to 23x in its immediate aftermath. As forward P/E ratios are based on forecasted growth in earnings, the story since 2021 has been a continued fall in software revenue growth expectations for software companies. Similarly, Bain reported (Bain & Company, Why Software Stocks Have dropped, February 2026) that public company SaaS year over year growth rates have fallen from 27% in 2021 to 10% as of February 2026.

Figure 6: Software Forward P/E vs. S&P 500

Source: Bloomberg Intelligence

We have seen a continued fall in both public market and private market SaaS valuation expectations, continued announcements of layoffs by major tech companies and reports of revenue shortfalls blamed on the SaaSpocalypse. Salesforce, Intuit, Atlassian, Snowflake and Service Now, among others, all lost value in Q1 2026 due to weaker forward guidance or analyst fears that agents will soon cannibalize SaaS seats.

At the same time, the Q1 investments in three leading AI companies (XAI, OpenAI, and Anthropic) totaled $160B of fresh funding, illustrating the flow of capital from SaaS to AI.

Exits: A Tale of Two Markets

Exit markets strongly reflect this significant shift in emphasis from traditional SaaS to native AI.

The SaaS IPO market is showing few signs of life. There were no enterprise SaaS or AI software IPOs in Q1’26. Relatively few SaaS companies have filed to go public later this year. And there are currently no blockbuster venture-backed SaaS IPOs in process apart from the possibility of public listings for Canva and Discord.

A key issue for SaaS companies is that many bellwether 2025 SaaS IPOs did not retain their value, including Figma, which has lost 80% of its first day value. Only a small percentage of 2025 non-AI IPOs retained their market value going into 2026, likely a major factor reducing investor enthusiasm for new SaaS issues.

The bar has been raised for technology IPOs, as E&Y, Crunchbase and others have noted. Bankers indicate that IPO candidates now require 1) at least $400M in ARR, 2) YoY growth rates of 30% and 3) profitability via the “Rule of 40” where revenue growth plus profit margin should exceed 40%.

While SaaS IPOs are depressed, in contrast, the market for native AI IPOs is exuberant. We are expecting several mega AI IPOs later in 2026 (possibly the largest IPOs in history). And the AI IPO boom may have already started. In May, Cerebras Systems (CESY) went public, the largest US technology IPO since Uber in 2019. It ended first day trading 70% above its offering price and had already raised its price twice during its roadshow. Not surprisingly, it was 20x oversubscribed. And at least five other potential mega AI IPOs are in various stages of readiness.

M&A in Q1 was similarly a tale of two different markets. In Q1 there were 620+ mostly low valued SaaS M&A. While far fewer in number, AI M&A deal counts increased 90% YoY in 2026 and were valued at many times the median value of SaaS transactions. AI-Native software companies were sold for 8x to 15x revenues whereas the top SaaS deals were sold at 4x to 5x ARR.

Private Equity accounted for 60% of traditional SaaS M&A exits, often buying assets at compressed multiples as part of PE consolidation or rollup strategies. The emergence of PE as the majority buyer of traditional SaaS companies (see SEG statistics) offers a significant guidepost for early-stage investors seeking to monetize portfolios of traditional SaaS assets.

The Case for the SaaSpocalypse

Growing skepticism about the viability of current SaaS economics; fundamental worries about agents replacing, first developers, then other workers; the decline in high-value IPO or M&A exits for SaaS companies; the fall in both public and private SaaS valuations; the inability to access public markets by SaaS unicorns and the many other SaaS companies filling our legacy portfolios; the shift in interest from traditional SaaS to agentic-powered software; and the AI money flood—none of these trends bode well for the long-term health of enterprise SaaS as currently conceived.

Counter Arguments to the SaaSpocalypse Narrative

The degree and persistence of harm to the now-traditional SaaS market won’t really be known for many months, at least until current trends stabilize and/or a new AI-integrated SaaS economic model emerges.

In any case, a fair discussion must acknowledge that the SaaSpocalypse is not universally accepted. Some think the SaaSpocalypse has been oversold and overhyped. Key arguments against the SaaSpocalypse include:

- After the February/March 2026 SaaS market bloodbath, traditional software indices have begun to recover (see the April/May segment of Figure 2).

- The dramatic decline of some SaaS metrics is often measured from their 2021 peak. Some observers, such as the author of this Data Insight, consider 2021 an atypical year of irrational exuberance and bubble-driven insanity. For some of us, post-2021 valuation declines were not only inevitable but, indeed, desirable.

- The 2026 decline in valuations was also influenced by constrained oil supply and other economic shocks from the Iran war, unrelated to the fundamental economic drivers of the software economy.

- While there has been a clear decline in the rate of growth of traditional SaaS, this is typical of maturing industries. Revenues still are increasing, though much more slowly, at least in the near term.

- Even if conceptually correct, the SaaSpocalypse will not occur all at once or everywhere. Most markets are pragmatic. Enterprise SaaS is likely to remain sticky for some time due to switching costs, sunk investments in training and operations, and the deeply entrenched culture developed by key enterprise software systems. Most major organizations, for example, use Salesforce for conceptualizing and managing sales and business development. Similarly, it is hard to imagine business operations without SAP or Oracle, or office work without Microsoft’s enterprise collaboration and database tools.

- Financial services, utilities, energy, healthcare, telecommunications, aerospace, transportation, intelligence and defense and other regulated industries extend trust to software vendors slowly, cautiously and only after extensive stress testing and vendor diligence. And in several of these markets, such as healthcare and aerospace, the design, development and maintenance of software is itself highly regulated. Weekend vibe coding is more likely to result in heavy fines than in deployable software updates.

- Once in, never out. Remember that 90% of the Fortune 500 continue to deploy COBOL, which still handles trillions of dollars in daily transactions.

- Major enterprise SaaS systems have high switching costs which might negate the value of replacing them anytime soon.

- Typical AI-developed software is currently a security nightmare and cannot be deployed without security-focused redesigns. Vibe-coding will no more address these concerns than “move fast, break things and ignore HIPAA” will ever become an accepted digital health protocol.

- It is likely that the SaaS panic is being magnified by concurrent hysteria, including the pushbacks against local data center projects and fear of the threatened Jobspocalypse.

- It is unlikely that SaaS will disappear. Indeed, many enterprise SaaS companies are actively integrating agentic and other AI technologies and changing their revenue models from per-seat to outcomes, value-based or usage-based metrics. Out of our legitimate SaaSpocalypse concerns is likely to emerge a new hybrid, AI-driven SaaS model for the enterprise.

Regardless of whatever new synthesis emerges, those early-stage investors best positioned for success are likely to be among the first to make changes to how they evaluate, invest and harvest the next generation of software deals. Part II of this data insight will examine how software investing is likely to evolve.

AUTHOR

Dr. Ronald Weissman/ Co-Chair, Enterprise/AI Group, Band of Angels / Chair Emeritus, Angel Capital Association