This is Part 2 of a two-part series. Part 1 reviews the pros and cons of the “SaaSpocalypse” and its impact on software valuations, exits and potential investor returns. Click here to read Part 1.

This Part 2 suggest how angels and other early-stage investors should deal with changes in the software investing landscape.

Key Issues for Early-Stage Investing:

- Angel returns have declined for the past several years and are dependent to a large degree on the health of the software sector

- Strong returns await healthy M&A and IPO markets, but the IPO outlook remains uncertain for older, pre-Native AI investee companies

- Agentic AI is poised to replace simple workflow applications popular with the first wave of AI chat applications

The current downturn in enterprise software and growing skepticism about SaaS require a rethinking of investment and exit strategies.

Regardless of the fate of existing SaaS systems, whether SaaSpocalypse Now! or SaaSpocalypse Never! AI is bringing permanent change to software development, validation, consumption, distribution, pricing and finance. And with these changes will come a long-term re-think about how we invest in software and harvest our returns.

Many of our existing SaaS companies are hard at work changing their core pricing from per-seat to usage or value-based methods. It is time for us as investors to re-examine our methods and adjust to the new realities that discussions about the SaaSpocalypse (whether pro or con) have highlighted.

Competitive Capital

It is already obvious that modern, AI-infused software development and marketing will require smaller teams. And with a reduced need for people comes a reduced need for capital.

While frontier technologists building foundation platforms like OpenAI and Anthropic will continue to hire large teams and vaporize unprecedented amounts of capital, the typical applications company using best of breed AI tools can reach key milestones for institutional funding with a two-to-five-person team and pre-seed and seed funding of $1M or less. Contrast this with the 15-to-25-person team and $5M to $15M required in the pre-AI era to achieve credible milestones. And growth beyond Seed or Series A, too, is often cheaper and far more efficient. Slack, with a team of 385 took 30 months to reach $100M in annual recurring revenue, impressive in its day. In contrast, Anysphere, developer of AI coding co-pilot, Cursor, required only two thirds of that time, 21 months, to reach $100M with a team of 20, only 6% of the team that built and marketed Slack. And Lovable (AI for coding and marketing) took only seven months to reach the $100M ARR mark, less than 25% of the time that Slack required, again, with a much smaller team. As the popular catchphrase notes, today “your MVP is essentially free.”

More teams than ever building significant products in record time will seek funding from seed investors. Given lower capital requirements, deal competition could be fierce among angels, micro-VCs, VCs, seed funds, hedge funds and other new entrants in early-stage capital markets.

Based on my conversations with CEOs, seed investors with a significant portfolio of real AI companies will be best positioned to win deals given their real experience with emergent AI frameworks and a culture influenced by AI dynamics. With easy access to capital those seeking investor partners may be as or more interested in ready access to a network of AI-ready customers and AI partners as they are in the capital itself. Early-stage investors will need to convince CEOs that they are already deeply embedded in the AI ecosystem and are not merely AI tourists.

Understanding today’s Moat

In traditional SaaS, one’s moat was often proprietary code, a superior user interface and user/vendor lock-in. Those are much less relevant in a world of open, collaborative multi-agent systems. The emerging moat for today’s AI-influenced software startups is a combination of deep proprietary domain data and/or deep vertical market expertise. Extensive knowledge of regulatory frameworks is also needed for credibility in those markets. Ensuring that startups possess the right domain knowledge will become a key diligence focus. Diligence must also validate core business model assumptions, including new pricing models and evolving customer buying preferences. And, of course, where relevant, a startup’s ability to adhere to regulatory oversight.

Speedy Decisions

It has never been easier to start a company, given available capital and a plethora of tools to build MVPs in days rather than months. Many entrepreneurs expect seed investors to evaluate deals as fast as their teams evolve their products. As the industry moves from funding foundation models to funding applications, new operational programs for efficient diligence may well separate investors who repeatedly win deals from the rest.

Sector Focus

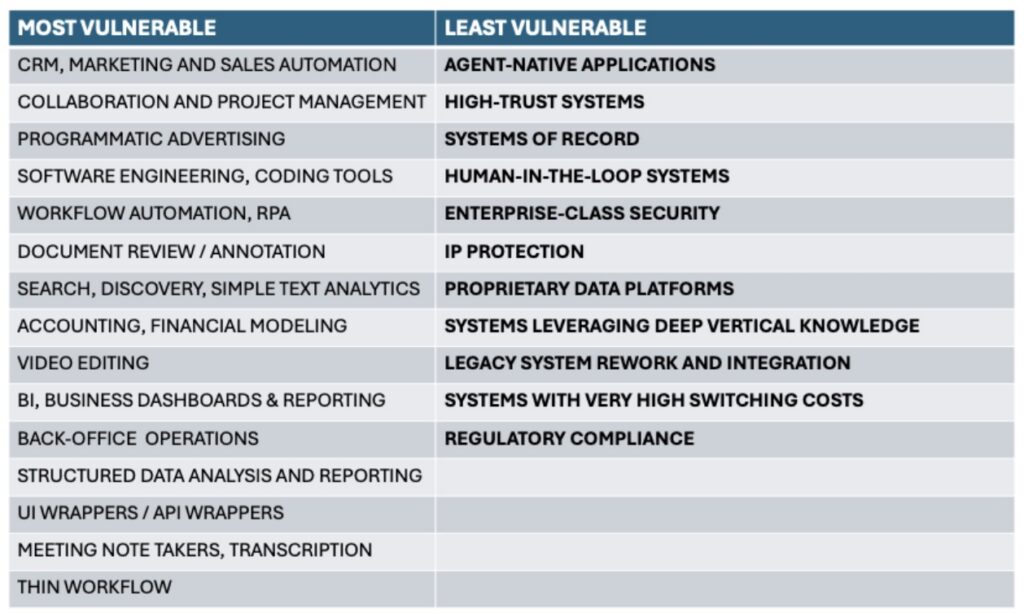

The movement from traditional pre-AI SaaS to AI-Native applications will create new classes of winners. Angel investors continuing to invest in enterprise applications should focus on sectors least vulnerable to AI disruption. Figure 1 enumerates software sectors likely to be less vulnerable or more vulnerable to AI disruption.

Figure 1: Relative AI Vulnerability of Software Sectors

Exits and Angels

Angel groups and VCs have seen a decline in the number and value of exits since the end of the pandemic. The emerging SaaSpocalypse is likely to make things worse, as SaaS software values are being compressed, resulting in lower value investor exits.

Based on the last several years of the ACA’s Angel Funder Reports, it is likely that 30% to 50% of angel portfolios are stocked with pre-Native AI software companies, having received investments prior to OpenAI’s emergence in November of 2022. Like VC-funded trapped unicorns unable to exit, many in our portfolios have, post-pandemic, seen anemic growth and are neither AI-native nor have had the resources to leverage AI meaningfully, beyond simple, hard to defend and moat-less LLM wrappers.

Of real benefit to angels, VCs have pioneered other methods of exits, including private equity sales of bargain priced companies appropriate for private equity turnarounds and rollups. We have also seen growth in secondary markets for portfolio company shares. Increasingly, both options are available to us. Angel groups should familiarize themselves with active private equity software buyers as well as with secondary market buyers of baskets of privately held portfolio companies and develop partnerships with leading, software-focused PE investors.

Key Takeaways: So, what can we do?

- To win deals, we need to embrace the emerging cultural norms of AI companies: let’s be where the deals are–at incubators, accelerators, seed funds and meet-ups focusing on AI. Let’s recruit AI native angels, well connected to our local AI ecosystems.

- If you are a software investor investing SaaS business models, focus on industries and classes of software less vulnerable to AI disruption. And ensure that your portfolio company is adopting alternatives to the traditional per-seat pricing model.

- Examine investment sectors powered by or adjacent to software such as HardTech, industrial applications, recycling, extractive tech, material science, defense, medical devices as well as the booming markets in physical AI, including digital twins. Partner with other specialty investors for access to these deals. Syndicate to raise enough capital to ensure that the syndicate gains a board seat and information rights.

- Be a data-driven angel, sensitive to the trends in exit valuations of different software/industry subsectors and changes in market dynamics. Sudden changes in market sentiment can turn former software heroes into zeros.

- Rethink how we do diligence for AI-related deals, focusing on new moats and on technical and business model diligence. Capitalize on deep domain knowledge within your network, as validating the existence of true AI moats requires it.

Whether an emerging threat or an overhyped fear, recognize that the SaaSpocalypse has fostered necessary conversations about how we value, invest and harvest our software portfolios. These conversations can lead to more considered, thoughtful software investing. These will make us better stewards of our current holdings as well as better investors in the next wave of AI-powered software.

AUTHOR

Dr. Ronald Weissman/ Co-Chair, Enterprise/AI Group, Band of Angels / Chair Emeritus, Angel Capital Association