The Investor Question: When A Life Science Company Goes Public, Did It Succeed?

For founders and management teams, the answer is often yes. An IPO brings capital, institutional validation, and the resources to fund programs that private markets cannot easily support. It creates currency for hiring and partnering. It can reduce near-term survival risk.

In the life science community, IPOs carry a powerful narrative. They signal credibility, access to capital, and durability in a capital-intensive industry. Many observers treat an IPO as a clear milestone of success.

For angels, the answer is less straightforward.

An IPO enables the sale of shares, subject to a lockup period, for management and investors. It does not determine the price at which angels sell those shares, the ownership that remains after dilution, or the time required to realize value. Liquidity exists. Return quality remains uncertain.

This article builds on Article 1 in a series examining how screening decisions translate into outcomes. Here, we focus on companies that BioAngels did not fund, but that later went public. We ask what those IPO paths reveal about exit, timing, and dilution realism for life science angels, and what that implies for effective screening.

Dataset and Scope

As a reminder, Mid Atlantic Bio Angels (BioAngels) has been analyzing data from 1,094 applications processed between 2012 and 2023, of which just over 1% were funded, to improve screening and diligence. For this analysis, we examined 23 BioAngels applicants that the group did not fund, but that later reached the public markets. These companies completed 11 traditional IPOs, 11 reverse mergers, and one SPAC transaction, mainly on U.S. exchanges.

The cohort is overwhelmingly therapeutics-driven. Twenty of the 23 companies develop drugs, typically as single-asset or narrowly focused pipeline programs rather than diversified platforms. Devices and diagnostics account for only three listings.

Most companies went public in early to mid-clinical development, most often in Phase 1 or Phase 2. Substantial clinical, regulatory, and commercial risk remained unresolved at listing. Traditional IPOs were often based on early human data but preceded pivotal trials and regulatory clarity. Non-traditional listings often occurred at similar or earlier stages and more frequently reflected financing constraints than a deliberate liquidity milestone.

Only a small minority had reached approval or early commercial activity at the time of listing. They did not change the overall pattern: most companies listed before durable commercial validation.

Pre-IPO financing relied heavily on dilutive equity. Traditional IPO companies often raised tens of millions of dollars before listing, materially compressing early ownership by the time shares became tradable. Non-traditional listings generally raised less capital in absolute terms, but dilution still eroded ownership as the company matured and approached value inflection points.

Non-dilutive funding played a limited role. Grants, government support, and early partnerships appeared in some cases, but they rarely offset dilution or reduced reliance on equity. Public market capital funding focused more on development and risk resolution than on scaling validated products.

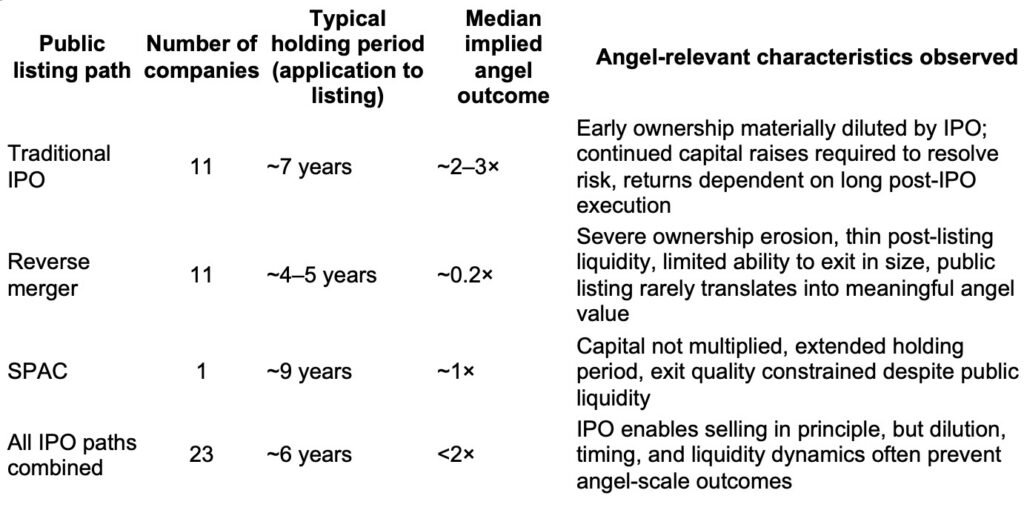

Summary of the IPO Dataset Analyzed

The table below summarizes how different public listing paths translated into holding period and implied angel outcomes.

FIGURE 1. COMPANY OUTCOMES BY type/duration and outcomes

Source: BioAngels internal analysis of life science companies that applied for funding between 2012 and 2023 (applied = 1,094; 18 funded).

We asked two questions. Would these IPO paths have produced meaningful angel-scale returns after dilution and time? And how should this affect the screening of companies that focus on IPOs as their exit path?

We used a simple, consistent ownership model across all existing companies to compare outcomes fairly. Rather than trying to reconstruct every cap table, we assumed a typical $250,000 BioAngels check buys about 5 percent at entry. From there, we modeled two to four priced rounds before exit, with 20 to 30 percent dilution per round. When a company came in already highly priced or clearly capital-intensive, especially certain therapeutics, we assumed heavier dilution earlier to reflect larger VC-style rounds. Over time, that typically reduces angel ownership to about 1 to 1.5 percent in standard cases and closer to 0.5 percent in heavier dilution cases. We then applied that final ownership to the exit value, using six-month post-IPO market caps or disclosed M&A values. This is a simplification, but it gives us a realistic, comparable way to understand returns. If anything, real-world ownership is often lower than we modeled, so the results are more likely to be generous than harsh.

Across this BioAngels dataset, IPO paths rarely produced meaningful angel returns. Capital requirements, dilution, and long timelines set the economics before listing. That pattern holds for traditional IPOs and is even more pronounced for reverse mergers and SPACs.

Traditional IPOs: Fragile Wins, Long Waits

Traditional IPOs did outperform non-traditional listings in this dataset, but the distribution remained narrow. The median implied angel outcome fell in the 2–3x range after roughly 7 years from application to listing. Most outcomes clustered between 1 and 4 times invested capital. Only one company generated meaningful returns.

Time did not rescue returns. Longer paths to IPO did not correlate with better outcomes. In several cases, the longest-held companies produced the weakest implied results.

Most companies IPO with unresolved material clinical and regulatory risks. Pivotal trials, regulatory clarity, and commercial validation still lie ahead. The IPO shifted financing risk to public markets. It did not eliminate it.

Companies are often listed after Phase 2 because early human data supported valuation, and capital needs escalated. Going public preserved company optionality and transferred funding to public investors. For angels, it extended dilution, volatility, and time to meaningful liquidity.

From a screening perspective, the issue is not whether a company can reach the public markets, but whether that path will produce acceptable returns within a realistic timeframe.

IPO-oriented applicants often signal this direction early. They anchor on public comparables, emphasize capital access, treat dilution as inevitable, and place less weight on strategic acquisition pathways. Acquisition logic may be secondary or underdeveloped. These signals do not necessarily predict scientific failure; they predict capital paths in which early ownership erodes and liquidity drifts further out.

Non-Traditional Listings: Faster to the Public, Worse for Angels

In the broader literature, reverse mergers and SPACs are often described as shortcuts to public markets, opportunistic alternatives during weak IPO windows, or tools that can rescue otherwise viable companies. Common cautions focus on governance, sponsor quality, and reputation. The investor economics receive less attention. In this dataset, reverse mergers and SPACs delivered materially worse economics.

Across 11 reverse mergers and one SPAC, the median implied angel outcome was roughly 0.2 times invested capital. Most cases failed to return capital. None produced an angel-scale win.

Shorter holding periods did not improve results. Many transactions created a ticker without creating usable liquidity. Trading depth remained thin. Institutional sponsorship was limited. Dilution often continued after listing, without a clear valuation inflection point.

Even when companies raised modest capital before listing, non-traditional paths still impaired meaningful outcomes. The problem was structural. Public capital funded survival more often than validation.

What IPOs Actually Reward in Life Sciences

Public markets reprice companies when uncertainty collapses in visible steps. Clinical milestones, regulatory clarity, commercial traction, platform validation, and disciplined capital use drive valuation changes far more than near-term profitability.

Profitability comes later. Clarity drives earlier repricing.

Angels typically face a six-month lockup after IPO. While they may not be required to hold beyond that period, the challenge is timing. In many cases, share prices declined materially by the time lockups expired, limiting the attractiveness of an early exit. Liquidity exists, but pricing may not compensate for prior dilution and risk.

That shifts the screening lens. The question is not whether a company can go public. The question is what an IPO would change for early ownership, dilution, and time to liquidity.

Angels must believe that beyond the whims of public markets, the company will resolve remaining risks within a defined horizon, that post-listing capital needs remain bounded, and that early ownership can remain economically meaningful.

At the angel stage, especially in therapeutics, those conditions are uncommon.

In this dataset, IPOs extended companies’ lives and funded programs more reliably than they preserved early investors’ returns. That does not make IPOs failures. It clarifies what they accomplish and what they do not.

Closing Reflection

IPOs play an essential role in the life science ecosystem. They fund innovation, extend company runways, and advance programs that private capital alone cannot sustain. For founders and later-stage investors, they are often rational and necessary.

For angels, IPOs create liquidity. They do not guarantee attractive returns. Shares become tradable, but dilution, timing, and post-listing volatility often limit the realization of value. And, when compared with exits via M&As, IPOs provided lower returns for angel investors, which only further validated the group’s assumption that life science company that performs well in a market segment that is attractive to strategics will be acquired before it reaches a stage when it would go public.

Screening discipline may not predict scientific success, but can recognize when a company’s most likely path pushes liquidity too far out or reduces ownership too far to justify early risk, which helps calibrate angel ROI expectations.

Key Takeaways

- In this cohort of BioAngels applicants that were declined but later went public, IPOs rarely translated into strong angel-scale returns after dilution and time.

- Traditional IPOs modestly outperformed reverse mergers and SPACs in this dataset, but median outcomes still clustered in the low single-digit multiple range after long holding periods.

- Most companies listed before pivotal risk was resolved and required continued financing after going public, further compressing early ownership.

- In these cases, return economics were largely determined before listing. Pre-IPO dilution and capital intensity shaped outcomes more than the IPO itself.

- For life science angels, IPO ambition should trigger ownership and timeline discipline. The key question is not whether a company can list, but whether early ownership will still matter when it does.

AUTHORS

- Alex Pederson (Member, Mid-Atlantic Bio Angels / BioAngels and Park City Angels)

- Yaniv Sneor (Founder, Mid-Atlantic Bio Angels / BioAngels)