Author: John Harbison, Chairman Emeritus of Tech Coast Angels and ACA Board Member.

Author: John Harbison, Chairman Emeritus of Tech Coast Angels and ACA Board Member.

The SEC’s Accredited Investor Definition has been in place since 1982. This requirement uses two measures of wealth as surrogates for sophistication as an investor, as well as attempts to mitigate possible negative consequences of what is admittedly a risky asset class. The current SEC regulation requires investors to meet one of the following criteria:

- Net worth over $1 million, excluding primary residence (individually or with spouse or partner)

- Income over $200,000 (individually) or $300,000 (with spouse or partner) in each of the prior two years, and reasonably expects the same for the current year

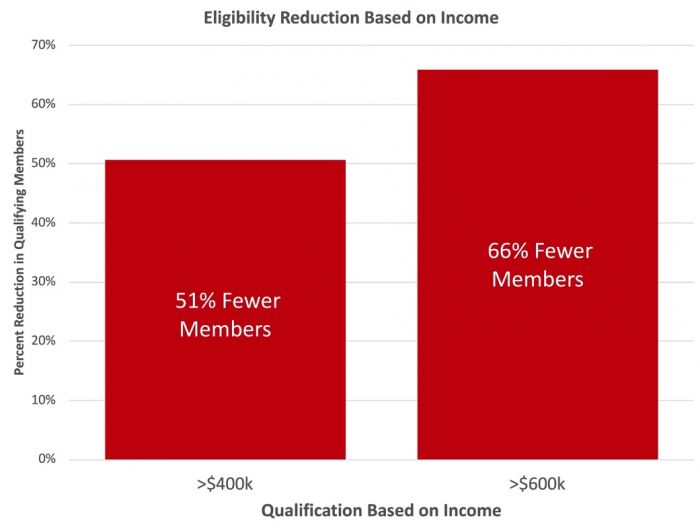

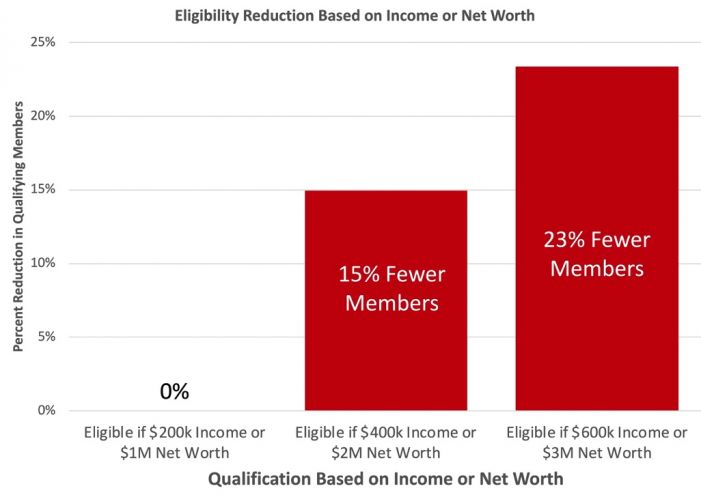

The SEC is currently considering making changes in those thresholds, possibly by indexing for inflation which would mean a tripling in the amounts. This raises a serious concern about how many currently active Angel Investors would no longer qualify to make investments in early-stage companies, and what that will do to stifle innovation and slow our economy. Such a change could trigger an existential crisis for early-stage companies who would become starved for much needed capital, since substantially more companies are funded by angel investors than by any other source.

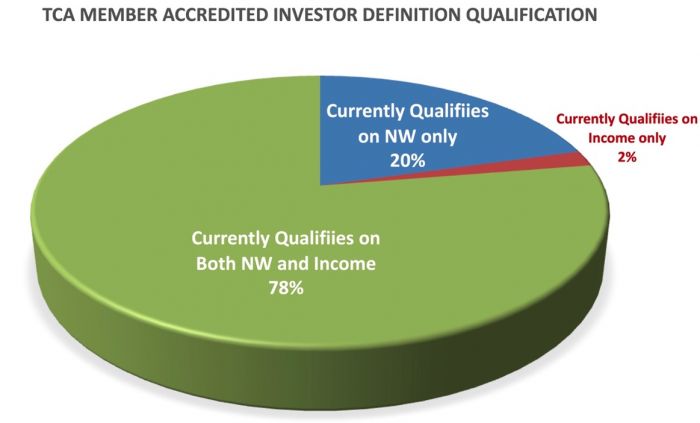

To understand this, Tech Coast Angels recently conducted a confidential survey of our 385 members, and 107 members responded – a healthy response rate. 78% of those responding members currently qualify on both the Net Worth and Income thresholds, with 20% qualifying only on the Net Worth threshold and 2% only on the Income threshold: