Angel Insights Blog

Friday, June 07, 2019

Angel Investing Exits: Base Hits to Home Runs

By: Ham Lord, Chairman of Launchpad Venture Group and Co-Founder of Seraf-investor.com and Christopher Mirabile, ACA Chair Emeritus, Managing Director at Launchpad Venture Group and Co-Founder of Seraf-investor.com

Note: This article is the eleventh in an ongoing series for angels new to investing. To learn more about building an angel portfolio, download this free eBook today – Angel 101: A Primer for Angel Investors or purchase our books at Amazon.com.

In the first two parts of this series on angel exits, we examined four different types of successful exits and four different types of failed exits. With our final article in the series we will address a few miscellaneous topics that are important for angel investors to understand as they build a diversified portfolio. And, for another take on angel exits, please read our article on an introduction to angels and exits.

Image by Tony Alter

Q: It has been said that you find out about your mistakes pretty quickly. What situations result in an exit occurring within the first 1 to 3 years?

As we discussed in the first post from this series, in our portfolio, these companies were usually characterized as early seed deals where a great idea didn’t pan out. The company raised a small amount of capital, but the technology didn’t work, or customers weren’t interested in buying for any one of a whole host of reasons. As seed investors, you decide to stop funding the company and the company can’t find any other investors. Although losing all your money in a seed deal doesn’t feel great, typically you put a small amount of money into the company at this stage. So your overall loss in time and money tends to be low. Remember, the only thing worse than a mistake, is an expensive mistake.

In some cases you don’t lose all your capital. If the founding team is solid, it’s not unusual for a larger company to acquire the failed company for their talented team and pay a modest amount to the early investors. Also, be aware of the tax benefits from IRS tax code section 1244 that might allow you to write off your loss versus your earned income instead of at the lower rate of capital gains.

Q: In your personal portfolio and the Launchpad portfolio, describe some of the successful exits? How long did they take? When is it OK to be patient?

I was an early investor in a company called SmartPak. SmartPak built the number one brand in the Equine market over a decade long time period. The company achieved strong, steady growth and was very capital efficient along the way. Management understood the importance of building a strong brand, and they did an incredible job of running a lean, efficient business. From initial investment to exit was about 12 years, but the return multiple was over 11x.

Launchpad’s successes span everything from a quick 1 year exit, to the typical 4 to 7 year exits, and finally 10+ year exits. As you would expect, the quick exits are predominantly 1.5x to 3x level of returns. The 4 to 7 year exits are clustered in a 3x to 8x level of return.

For the 10+ year type of exit, I believe it’s okay to be patient as long as the company hasn’t raised a lot of capital. For companies that are capital efficient, there isn’t a significant overhang from the preference stack (i.e. preferred stock liquidation preferences and dividends). As the clock ticks, dividends can really add up, especially when a company raises $10M or more over time. A large preference stack will cut severely into returns for early investors. At Launchpad, we have one long term investment that raised around $1M in angel money at a low valuation. Based on their current financial metrics, the company should be able to exit with greater than a 10x multiple for the investors.

Q: There are lots of stories in the press about the big wins such as Facebook and Google. How common are those exits? Are those kinds of exits limited to consumer internet, or do they happen in other industries?

Returns like 1500x for early eBay investors are an incredibly rare thing, but still fuel the dreams and provide the justifications for many investments, particularly in consumer web and consumer mobile. But these gold rush type returns are super rare and really only associated with massive disruptions like quickly going from no broadband to ubiquitous broadband or slow expensive wireless to fast cheap wireless.

Success in consumer markets easily overshadows success in other industries. However, there are other areas where angel investors should consider. For example, enterprise software companies such as Salesforce.com and Workday have market caps well in excess of $10B. In healthcare, there are a number of successful companies such as Athenahealth, Gilead and Celgene. In some cases, the companies are capital efficient (e.g. Athenahealth), but in others (e.g. Gilead) they are not. So early investors in the life sciences need to be aware of the enormous capital required to turn out a successful company.

Q: If you built a portfolio of 10 companies, what should you expect?

Assuming you are an angel investor who puts time and effort into building your 10 company portfolio by performing due diligence and adding human capital to support your investments, you should have the following expectations.

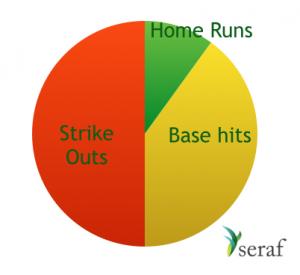

A rough estimate for your portfolio will include 5 failed companies, 4 base hits and 1 home run. Let’s break this down a bit further and understand what this will mean for your returns. With the 5 failures, you can expect little if any capital returned. You will have some tax benefits on the losses, but they will add up to around 20-30% of your original investment

Base hits describe exits anywhere from 1x to 10x of your original investment. As we discussed in a previous question, quick exits will result in a 1.5x to 3x return of capital and the other exits should cluster in the 3x to 8x range.

Your portfolio’s 1 home run should be somewhere greater than a 10x return. Assuming you allocated the same amount of capital to all 10 companies, this company will return all the capital that you invested in the original 10 companies. Think of this exit as ‘returning your fund’. But, how you do overall is now driven by how your base hits do. A couple of 5x returns and a couple of 3x returns will help you generate overall fund returns of at least 2.5x your original capital.

Want to learn more about building an angel portfolio and developing the key skills needed to make great investments? Download Angel 101: A Primer for Angel Investors and Angel Exits: Perspectives and Techniques for Maximizing Investment Returns, or purchase our books at Amazon.com.

Tags: