Angel Insights Blog

Friday, May 15, 2015

2014 Pre-Money Valuation of Seed Stage Angel Deals

By Bill Payne, Frontier Angel Funds

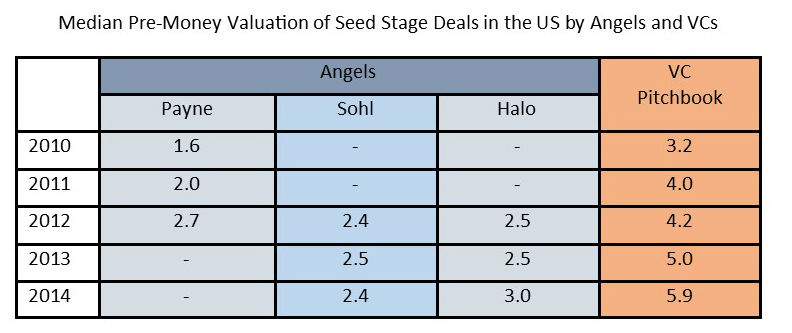

The median pre-money valuation of seed stage deals has increased since 2010, as the US economy has emerged from the recent recession. The following table shows the pre-money valuation of seed stage deals from several sources over the past five years:

Payne’s survey data was provided by 30 angel groups from all regions of the US Sohl’s data is published annually by the Center for Venture Research at the University of New Hampshire. The Halo Reports are published quarterly by the Angel Resource Institute for deals done by angel groups. Pitchbook data is from 1H 2015 VC Valuations and Trends

There appears to be general agreement that the pre-money valuation of seed stage deals has increased significantly since 2010 and perhaps doubled. We also see that the valuation of seed stage deals funded by VCs is about twice that of angel deals. This data prompts several questions:

- Why is the pre-money valuation of seed stage deals higher for VC-funded companies than for angel-funded companies? I believe there are two components to this answer:

- The round size for seed stage VC deals is higher than for angel-funded seed stage deals.

- The Pitchbook data is dominated by VC deals done in Silicon Valley and other highly competitive markets where pre-money valuations have been shown to be higher than elsewhere in the country (see more below).

- Why are angel valuations increasing? Angels invest monies from their personal accounts and generally commit 3-10% of their assets to the angel asset class. When the remainder of their portfolios are doing poorly (during a recession), they are less likely to invest in higher risk deals (such as startup companies). Yet entrepreneurs are still starting companies. Demand remains strong or increases during a recession while supply of angel capital decreases. Consequently, prices fall during a recession, and that is exactly what happened in 2008-2010. We are now seeing increased pricing as the country emerges from the recession.

- Is there much variation in pre-money valuation by business sector? The Payne survey of angel groups in 2012 found less than 20% variation in the mean valuation for sectors such as software, life science and clean tech. Pitchbook’s 1H 2015 VC Valuations and Trends shows even less variation among business sectors for seed stage VC deals.

- Does the valuation of startup deals vary by location? This same Pitchbook report shows that the pre-money valuation of early stage deals is currently twice as high in Silicon Valley and Los Angeles than in Austin or Denver/Boulder, which is in agreement with earlier work by Payne, reported in Why Does Startup Pricing Vary by Location?

Tags: