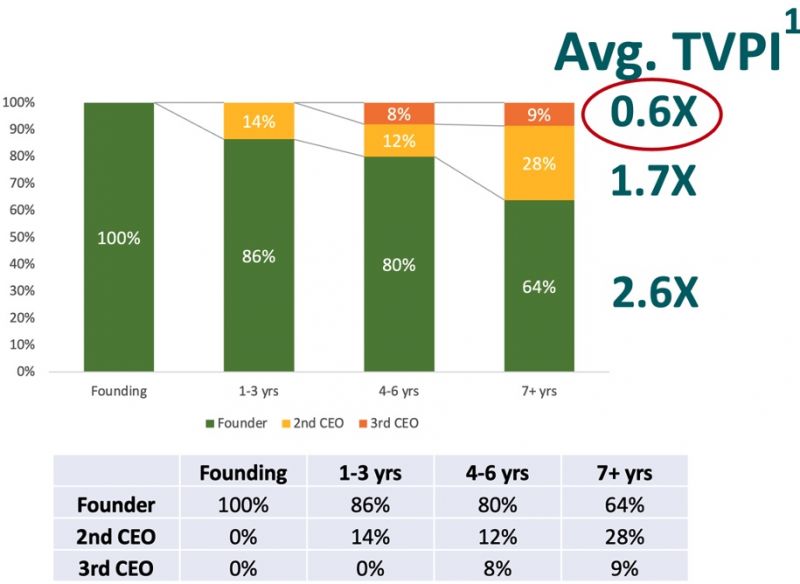

In 64% of our companies, the CEO made it more than seven years. Those companies had by far the best return multiples. We saw an average return multiple of 2.6X with single CEO companies. The 28% of companies experiencing just one CEO change were still a winning proposition, showing a 1.7X return multiple as a group, but they were still a much weaker outcome overall – 35% lower. And the companies that needed two CEO changes were money losing as a group, showing an average return multiple of just 0.6X. That is a marked difference; chose a great CEO and you are looking at an average return approaching 3X. Back the wrong CEO and you are lucky to get your money back.

What actionable lessons can we take away from this data? Well, before we draw conclusions, we need to acknowledge three things. First, correlation and causation are not the same and one needs to be careful assuming a causal connection when it could be correlational or two seemingly connected factors which are actually independently connected to a third factor. For example, in this case, common sense dictates that if the CEO is being changed, things are already not going perfectly smoothly. However, I would argue that the converse is also somewhat true – if the CEO is good, that is one less thing to go wrong and therefore you have a better probability of success and higher returns.

Second, it is possible that the reason we saw lower rates of CEO change is that angels are just more patient about replacing CEOs or lack the political power (or legal means) to do so. There is probably some truth to that as a general proposition, but it may not entirely explain the lower rate of CEO changes in our case. Launchpad strongly prefers to lead its rounds, and typically does, and we virtually always take a board or observer seat. We also place fairly large bets and tend to follow on fairly strongly over time, so it is not uncommon for us to hold 10% or more of a company in the later years. So we often have a voice at the table and some voting clout to back it up. And, sure enough, throughout our 20+ year history, we have a track record of initiating CEO changes where we felt they were necessary.

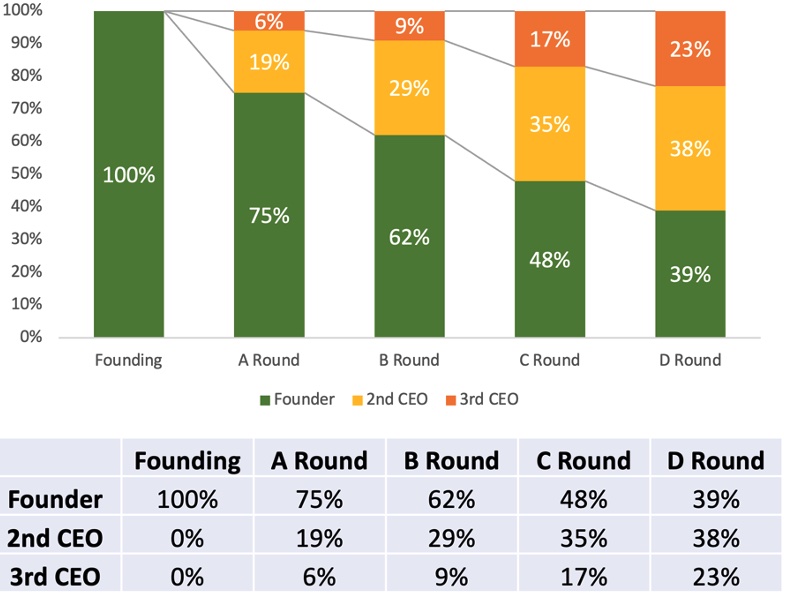

Third, we must acknowledge the difficult dynamics of attracting new CEOs to young companies with shaky financials. It stands to reason that the only companies that are going to be able to attract good replacement CEOs are going to be the solid companies with more potential. Again, that may be the case as a general matter, but it does not fully explain our data. If it is not possible to attract new CEOs to angel backed companies, how were we able to do it 36% of the time? And even with the ones that were extra messy, how were we able to attract a THIRD CEO nearly 10% of the time? Certainly, smaller angel-backed companies may not have quite as easy a time replacing CEOs as bigger more cash-rich companies, but they definitely can do it.

So for us, the three take-aways from this data were clear. The first conclusion was that the time we spend in diligence really evaluating founding teams, and especially founding CEOs, is well worth it. Finding good CEOs who can scale themselves as they grow a company is correlated with much higher average returns. The second conclusion is that even if we don’t nail it on the CEO choice, we might still be OK if the opportunity is good and the CEO is decent enough to make some progress before getting replaced. Having to replace a CEO when things are going OK still costs a bit, knocking nearly a third off your returns, but is not fatal. The third conclusion is that when we bet wrong on the CEO, and the company goes on to flounder and cannot attract a “keeper” replacement CEO, we are done for, and, on average, are going to lose money.

By Christopher Mirabile, ACA Chair Emeritus & Launchpad Venture Group Executive Chair

By Christopher Mirabile, ACA Chair Emeritus & Launchpad Venture Group Executive Chair